60. Globalization and Cycles#

Co-authored with Chase Coleman

60.1. Overview#

In this lecture, we review the paper Globalization and Synchronization of Innovation Cycles by Kiminori Matsuyama, Laura Gardini and Iryna Sushko.

This model helps us understand several interesting stylized facts about the world economy.

One of these is synchronized business cycles across different countries.

Most existing models that generate synchronized business cycles do so by assumption, since they tie output in each country to a common shock.

They also fail to explain certain features of the data, such as the fact that the degree of synchronization tends to increase with trade ties.

By contrast, in the model we consider in this lecture, synchronization is both endogenous and increasing with the extent of trade integration.

In particular, as trade costs fall and international competition increases, innovation incentives become aligned and countries synchronize their innovation cycles.

60.1.1. Background#

The model builds on work by Judd [Jud85], Deneckner and Judd [DJ92] and Helpman and Krugman [HK85] by developing a two country model with trade and innovation.

On the technical side, the paper introduces the concept of coupled oscillators to economic modeling.

As we will see, coupled oscillators arise endogenously within the model.

Below we review the model and replicate some of the results on synchronization of innovation across countries.

60.2. Key Ideas#

It is helpful to begin with an overview of the mechanism.

60.2.1. Innovation Cycles#

As discussed above, two countries produce and trade with each other.

In each country, firms innovate, producing new varieties of goods and, in doing so, receiving temporary monopoly power.

Imitators follow and, after one period of monopoly, what had previously been new varieties now enter competitive production.

Firms have incentives to innovate and produce new goods when the mass of varieties of goods currently in production is relatively low.

In addition, there are strategic complementarities in the timing of innovation.

Firms have incentives to innovate in the same period, so as to avoid competing with substitutes that are competitively produced.

This leads to temporal clustering in innovations in each country.

After a burst of innovation, the mass of goods currently in production increases.

However, goods also become obsolete, so that not all survive from period to period.

This mechanism generates a cycle, where the mass of varieties increases through simultaneous innovation and then falls through obsolescence.

60.2.2. Synchronization#

In the absence of trade, the timing of innovation cycles in each country is decoupled.

This will be the case when trade costs are prohibitively high.

If trade costs fall, then goods produced in each country penetrate each other’s markets.

As illustrated below, this leads to synchonization of business cycles across the two countries.

60.3. Model#

Let’s write down the model more formally.

(The treatment is relatively terse since full details can be found in the original paper)

Time is discrete with \(t = 0, 1, \dots\).

There are two countries indexed by \(j\) or \(k\).

In each country, a representative household inelastically supplies \(L_j\) units of labor at wage rate \(w_{j, t}\).

Without loss of generality, it is assumed that \(L_{1} \geq L_{2}\).

Households consume a single nontradeable final good which is produced competitively.

Its production involves combining two types of tradeable intermediate inputs via

Here \(X^o_{k, t}\) is a homogeneous input which can be produced from labor using a linear, one-for-one technology.

It is freely tradeable, competitively supplied, and homogeneous across countries.

By choosing the price of this good as numeraire and assuming both countries find it optimal to always produce the homogeneous good, we can set \(w_{1, t} = w_{2, t} = 1\).

The good \(X_{k, t}\) is a composite, built from many differentiated goods via

Here \(x_{k, t}(\nu)\) is the total amount of a differentiated good \(\nu \in \Omega_t\) that is produced.

The parameter \(\sigma > 1\) is the direct partial elasticity of substitution between a pair of varieties and \(\Omega_t\) is the set of varieties available in period \(t\).

We can split the varieties into those which are supplied competitively and those supplied monopolistically; that is, \(\Omega_t = \Omega_t^c + \Omega_t^m\).

60.3.1. Prices#

Demand for differentiated inputs is

Here

\(p_{k, t}(\nu)\) is the price of the variety \(\nu\) and

\(P_{k, t}\) is the price index for differentiated inputs in \(k\), defined by

The price of a variety also depends on the origin, \(j\), and destination, \(k\), of the goods because shipping varieties between countries incurs an iceberg trade cost \(\tau_{j,k}\).

Thus the effective price in country \(k\) of a variety \(\nu\) produced in country \(j\) becomes \(p_{k, t}(\nu) = \tau_{j,k} \, p_{j, t}(\nu)\).

Using these expressions, we can derive the total demand for each variety, which is

where

It is assumed that \(\tau_{1,1} = \tau_{2,2} = 1\) and \(\tau_{1,2} = \tau_{2,1} = \tau\) for some \(\tau > 1\), so that

The value \(\rho \in [0, 1)\) is a proxy for the degree of globalization.

Producing one unit of each differentiated variety requires \(\psi\) units of labor, so the marginal cost is equal to \(\psi\) for \(\nu \in \Omega_{j, t}\).

Additionally, all competitive varieties will have the same price (because of equal marginal cost), which means that, for all \(\nu \in \Omega^c\),

Monopolists will have the same marked-up price, so, for all \(\nu \in \Omega^m\) ,

Define

Using the preceding definitions and some algebra, the price indices can now be rewritten as

The symbols \(N_{j, t}^c\) and \(N_{j, t}^m\) will denote the measures of \(\Omega^c\) and \(\Omega^m\) respectively.

60.3.2. New Varieties#

To introduce a new variety, a firm must hire \(f\) units of labor per variety in each country.

Monopolist profits must be less than or equal to zero in expectation, so

With further manipulations, this becomes

60.3.3. Law of Motion#

With \(\delta\) as the exogenous probability of a variety becoming obsolete, the dynamic equation for the measure of firms becomes

We will work with a normalized measure of varieties

We also use \(s_j := \frac{L_j}{L_1 + L_2}\) to be the share of labor employed in country \(j\).

We can use these definitions and the preceding expressions to obtain a law of motion for \(n_t := (n_{1, t}, n_{2, t})\).

In particular, given an initial condition, \(n_0 = (n_{1, 0}, n_{2, 0}) \in \mathbb{R}_{+}^{2}\), the equilibrium trajectory, \(\{ n_t \}_{t=0}^{\infty} = \{ (n_{1, t}, n_{2, t}) \}_{t=0}^{\infty}\), is obtained by iterating on \(n_{t+1} = F(n_t)\) where \(F : \mathbb{R}_{+}^{2} \rightarrow \mathbb{R}_{+}^{2}\) is given by

Here

while

and \(h_j(n_k)\) is defined implicitly by the equation

Rewriting the equation above gives us a quadratic equation in terms of \(h_j(n_k)\).

Since we know \(h_j(n_k) > 0\) then we can just solve the quadratic equation and return the positive root.

This gives us

60.4. Simulation#

Let’s try simulating some of these trajectories.

We will focus in particular on whether or not innovation cycles synchronize across the two countries.

As we will see, this depends on initial conditions.

For some parameterizations, synchronization will occur for “most” initial conditions, while for others synchronization will be rare.

Here’s the main body of code.

using Pkg; pkgs = ["Plots"]; all(haskey.(Ref(Pkg.project().dependencies), pkgs)) || Pkg.add(pkgs)

using LinearAlgebra, Statistics, Plots

function h_j(j, nk, s1, s2, theta, delta, rho)

# Find out who's h we are evaluating

if j == 1

sj = s1

sk = s2

else

sj = s2

sk = s1

end

# Coefficients on the quadratic a x^2 + b x + c = 0

a = 1.0

b = ((rho + 1 / rho) * nk - sj - sk)

c = (nk * nk - (sj * nk) / rho - sk * rho * nk)

# Positive solution of quadratic form

root = (-b + sqrt(b * b - 4 * a * c)) / (2 * a)

return root

end

function DLL(n1, n2, s1_rho, s2_rho, s1, s2, theta, delta, rho)

(n1 <= s1_rho) && (n2 <= s2_rho)

end

function DHH(n1, n2, s1_rho, s2_rho, s1, s2, theta, delta, rho)

(n1 >= h_j(1, n2, s1, s2, theta, delta, rho)) &&

(n2 >= h_j(2, n1, s1, s2, theta, delta, rho))

end

function DHL(n1, n2, s1_rho, s2_rho, s1, s2, theta, delta, rho)

(n1 >= s1_rho) && (n2 <= h_j(2, n1, s1, s2, theta, delta, rho))

end

function DLH(n1, n2, s1_rho, s2_rho, s1, s2, theta, delta, rho)

(n1 <= h_j(1, n2, s1, s2, theta, delta, rho)) && (n2 >= s2_rho)

end

function one_step(n1, n2, s1_rho, s2_rho, s1, s2, theta, delta, rho)

# Depending on where we are, evaluate the right branch

if DLL(n1, n2, s1_rho, s2_rho, s1, s2, theta, delta, rho)

n1_tp1 = delta * (theta * s1_rho + (1 - theta) * n1)

n2_tp1 = delta * (theta * s2_rho + (1 - theta) * n2)

elseif DHH(n1, n2, s1_rho, s2_rho, s1, s2, theta, delta, rho)

n1_tp1 = delta * n1

n2_tp1 = delta * n2

elseif DHL(n1, n2, s1_rho, s2_rho, s1, s2, theta, delta, rho)

n1_tp1 = delta * n1

n2_tp1 = delta * (theta * h_j(2, n1, s1, s2, theta, delta, rho) +

(1 - theta) * n2)

elseif DLH(n1, n2, s1_rho, s2_rho, s1, s2, theta, delta, rho)

n1_tp1 = delta * (theta * h_j(1, n2, s1, s2, theta, delta, rho) +

(1 - theta) * n1)

n2_tp1 = delta * n2

end

return n1_tp1, n2_tp1

end

function new_n1n2(n1_0, n2_0, s1_rho, s2_rho, s1, s2, theta, delta, rho)

one_step(n1_0, n2_0, s1_rho, s2_rho, s1, s2, theta, delta, rho)

end

function pers_till_sync(n1_0, n2_0, s1_rho, s2_rho, s1, s2, theta, delta, rho,

maxiter, npers)

# Initialize the status of synchronization

synchronized = false

pers_2_sync = maxiter

iters = 0

nsync = 0

while (!synchronized) && (iters < maxiter)

# Increment the number of iterations and get next values

iters += 1

n1_t, n2_t = new_n1n2(n1_0, n2_0, s1_rho, s2_rho, s1, s2, theta, delta,

rho)

# Check whether same in this period

if abs(n1_t - n2_t) < 1e-8

nsync += 1

# If not, then reset the nsync counter

else

nsync = 0

end

# If we have been in sync for npers then stop and countries

# became synchronized nsync periods ago

if nsync > npers

synchronized = true

pers_2_sync = iters - nsync

end

n1_0, n2_0 = n1_t, n2_t

end

return synchronized, pers_2_sync

end

function create_attraction_basis(s1_rho, s2_rho, s1, s2, theta, delta, rho,

maxiter, npers, npts)

# Create unit range with npts

synchronized, pers_2_sync = false, 0

unit_range = range(0.0, 1.0, length = npts)

# Allocate space to store time to sync

time_2_sync = zeros(npts, npts)

# Iterate over initial conditions

for (i, n1_0) in enumerate(unit_range)

for (j, n2_0) in enumerate(unit_range)

synchronized, pers_2_sync = pers_till_sync(n1_0, n2_0, s1_rho,

s2_rho, s1, s2, theta,

delta, rho, maxiter,

npers)

time_2_sync[i, j] = pers_2_sync

end

end

return time_2_sync

end

# model

function MSGSync(s1 = 0.5, theta = 2.5, delta = 0.7, rho = 0.2)

# Store other cutoffs and parameters we use

s2 = 1 - s1

s1_rho = min((s1 - rho * s2) / (1 - rho), 1)

s2_rho = 1 - s1_rho

return (; s1, s2, s1_rho, s2_rho, theta, delta, rho)

end

function simulate_n(model, n1_0, n2_0, T)

(; s1, s2, theta, delta, rho, s1_rho, s2_rho) = model

# Allocate space

n1 = zeros(T)

n2 = zeros(T)

# Simulate for T periods

for t in 1:T

# Get next values

n1[t], n2[t] = n1_0, n2_0

n1_0, n2_0 = new_n1n2(n1_0, n2_0, s1_rho, s2_rho, s1, s2, theta, delta,

rho)

end

return n1, n2

end

function pers_till_sync(model, n1_0, n2_0, maxiter = 500, npers = 3)

(; s1, s2, theta, delta, rho, s1_rho, s2_rho) = model

return pers_till_sync(n1_0, n2_0, s1_rho, s2_rho, s1, s2,

theta, delta, rho, maxiter, npers)

end

function create_attraction_basis(model;

maxiter = 250,

npers = 3,

npts = 50)

(; s1, s2, theta, delta, rho, s1_rho, s2_rho) = model

ab = create_attraction_basis(s1_rho, s2_rho, s1, s2, theta, delta,

rho, maxiter, npers, npts)

return ab

end

create_attraction_basis (generic function with 2 methods)

60.4.1. Time Series of Firm Measures#

We write a short function below that exploits the preceding code and plots two time series.

Each time series gives the dynamics for the two countries.

The time series share parameters but differ in their initial condition.

Here’s the function

function plot_timeseries(n1_0, n2_0, s1 = 0.5, theta = 2.5, delta = 0.7,

rho = 0.2)

model = MSGSync(s1, theta, delta, rho)

n1, n2 = simulate_n(model, n1_0, n2_0, 25)

return [n1 n2]

end

# Create figures

data_ns = plot_timeseries(0.15, 0.35)

data_s = plot_timeseries(0.4, 0.3)

plot(data_ns, title = "Not Synchronized", legend = false)

plot(data_s, title = "Synchronized", legend = false)

In the first case, innovation in the two countries does not synchronize.

In the second case different initial conditions are chosen, and the cycles become synchronized.

60.4.2. Basin of Attraction#

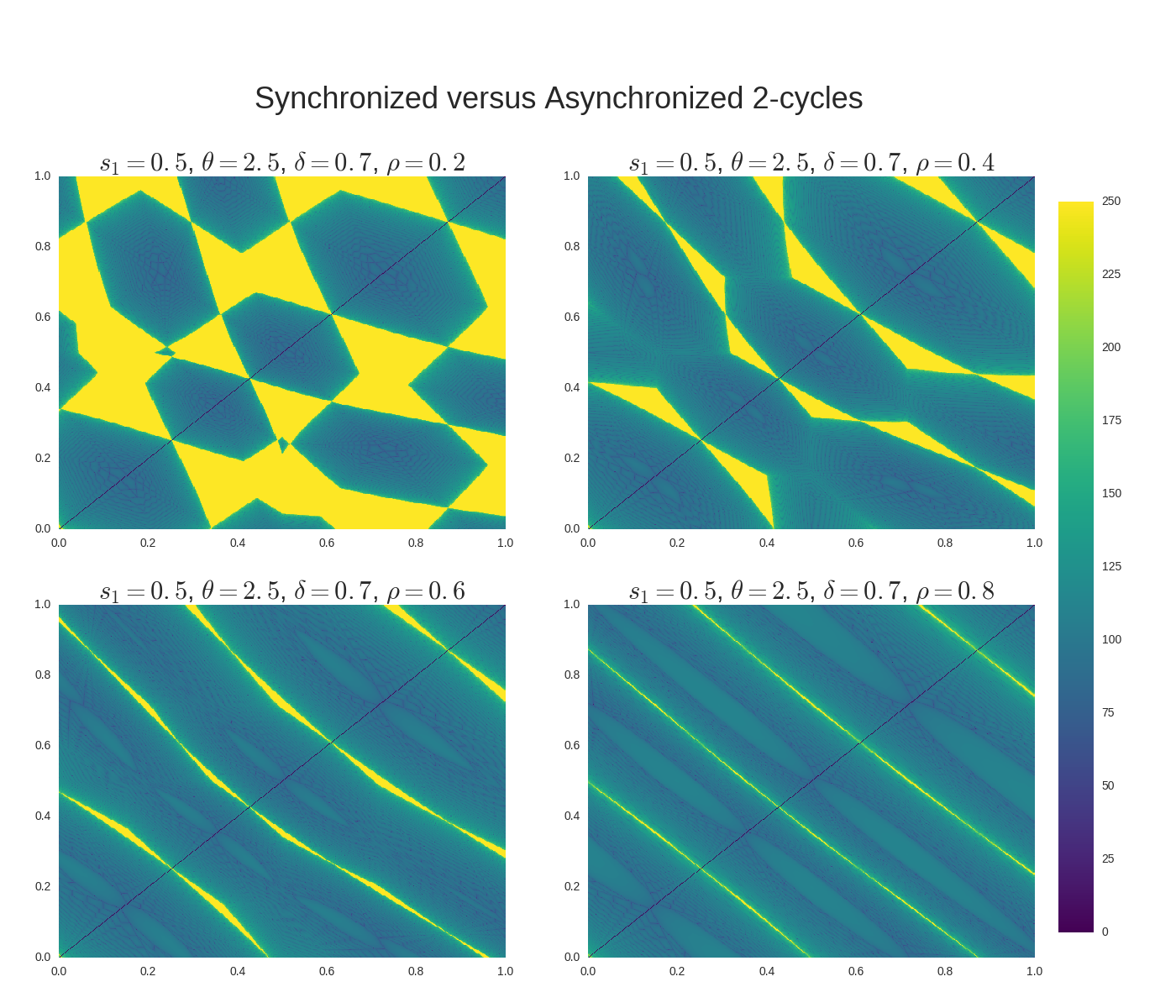

Next let’s study the initial conditions that lead to synchronized cycles more systematically.

We generate time series from a large collection of different initial conditions and mark those conditions with different colors according to whether synchronization occurs or not.

The next display shows exactly this for four different parameterizations (one for each subfigure).

Dark colors indicate synchronization, while light colors indicate failure to synchronize.

As you can see, larger values of \(\rho\) translate to more synchronization.

You are asked to replicate this figure in the exercises.

60.5. Exercises#

60.5.1. Exercise 1#

Replicate the figure shown above by coloring initial conditions according to whether or not synchronization occurs from those conditions.

60.6. Solutions#

60.6.1. Exercise 1#

function plot_attraction_basis(s1 = 0.5, theta = 2.5, delta = 0.7, rho = 0.2;

npts = 250)

# Create attraction basis

unitrange = range(0, 1, length = npts)

model = MSGSync(s1, theta, delta, rho)

ab = create_attraction_basis(model, npts = npts)

plt = Plots.heatmap(ab, legend = false)

end

plot_attraction_basis (generic function with 5 methods)

params = [[0.5, 2.5, 0.7, 0.2],

[0.5, 2.5, 0.7, 0.4],

[0.5, 2.5, 0.7, 0.6],

[0.5, 2.5, 0.7, 0.8]]

plots = (plot_attraction_basis(p...) for p in params)

plot(plots..., size = (1000, 1000))