33. Job Search IV: Modeling Career Choice#

33.1. Overview#

Next we study a computational problem concerning career and job choices.

The model is originally due to Derek Neal [Nea99].

This exposition draws on the presentation in [LS18], section 6.5.

33.1.1. Model features#

Career and job within career both chosen to maximize expected discounted wage flow.

Infinite horizon dynamic programming with two state variables.

using Pkg; pkgs = ["Distributions", "LaTeXStrings", "NLsolve", "Plots"]; all(haskey.(Ref(Pkg.project().dependencies), pkgs)) || Pkg.add(pkgs)

using LinearAlgebra, Statistics, NLsolve

using Distributions, LaTeXStrings, Plots, Random

33.2. Model#

In what follows we distinguish between a career and a job, where

a career is understood to be a general field encompassing many possible jobs, and

a job is understood to be a position with a particular firm

For workers, wages can be decomposed into the contribution of job and career

\(w_t = \theta_t + \epsilon_t\), where

\(\theta_t\) is contribution of career at time \(t\)

\(\epsilon_t\) is contribution of job at time \(t\)

At the start of time \(t\), a worker has the following options

retain a current (career, job) pair \((\theta_t, \epsilon_t)\) — referred to hereafter as “stay put”

retain a current career \(\theta_t\) but redraw a job \(\epsilon_t\) — referred to hereafter as “new job”

redraw both a career \(\theta_t\) and a job \(\epsilon_t\) — referred to hereafter as “new life”

Draws of \(\theta\) and \(\epsilon\) are independent of each other and past values, with

\(\theta_t \sim F\)

\(\epsilon_t \sim G\)

Notice that the worker does not have the option to retain a job but redraw a career — starting a new career always requires starting a new job.

A young worker aims to maximize the expected sum of discounted wages.

subject to the choice restrictions specified above.

Let \(V(\theta, \epsilon)\) denote the value function, which is the maximum of (33.1) over all feasible (career, job) policies, given the initial state \((\theta, \epsilon)\).

The value function obeys

where

Evidently \(I\), \(II\) and \(III\) correspond to “stay put”, “new job” and “new life”, respectively.

33.2.1. Parameterization#

As in [LS18], section 6.5, we will focus on a discrete version of the model, parameterized as follows:

both \(\theta\) and \(\epsilon\) take values in the set

linspace(0, B, N)— an even grid of \(N\) points between \(0\) and \(B\) inclusive\(N = 50\)

\(B = 5\)

\(\beta = 0.95\)

The distributions \(F\) and \(G\) are discrete distributions

generating draws from the grid points linspace(0, B, N).

A very useful family of discrete distributions is the Beta-binomial family, with probability mass function

Interpretation:

draw \(q\) from a \(\beta\) distribution with shape parameters \((a, b)\)

run \(n\) independent binary trials, each with success probability \(q\)

\(p(k \,|\, n, a, b)\) is the probability of \(k\) successes in these \(n\) trials

Nice properties:

very flexible class of distributions, including uniform, symmetric unimodal, etc.

only three parameters

Here’s a figure showing the effect of different shape parameters when \(n=50\).

using LaTeXStrings, Plots, Distributions, Random

n = 50

a_vals = [0.5, 1, 100]

b_vals = [0.5, 1, 100]

plt = plot()

for (a, b) in zip(a_vals, b_vals)

ab_label = L"$a = %$a, b = %$b$"

dist = BetaBinomial(n, a, b)

plot!(plt, 0:n, pdf.(dist, support(dist)), label = ab_label)

end

plt

Implementation:

The code for solving the DP problem described above is found below:

function CareerWorkerProblem(; beta = 0.95,

B = 5.0,

N = 50,

F_a = 1.0,

F_b = 1.0,

G_a = 1.0,

G_b = 1.0)

theta = range(0, B, length = N)

epsilon = copy(theta)

dist_F = BetaBinomial(N - 1, F_a, F_b)

dist_G = BetaBinomial(N - 1, G_a, G_b)

F_probs = pdf.(dist_F, support(dist_F))

G_probs = pdf.(dist_G, support(dist_G))

F_mean = sum(theta .* F_probs)

G_mean = sum(epsilon .* G_probs)

return (; beta, N, B, theta, epsilon, F_probs, G_probs, F_mean, G_mean)

end

function update_bellman!(cp, v, out; ret_policy = false)

# new life. This is a function of the distribution parameters and is

# always constant. No need to recompute it in the loop

v3 = (cp.G_mean + cp.F_mean .+ cp.beta .* cp.F_probs' * v * cp.G_probs)[1] # do not need 1 element array

for j in 1:(cp.N)

for i in 1:(cp.N)

# stay put

v1 = cp.theta[i] + cp.epsilon[j] + cp.beta * v[i, j]

# new job

v2 = (cp.theta[i] .+ cp.G_mean .+ cp.beta .* v[i, :]' * cp.G_probs)[1] # do not need a single element array

if ret_policy

if v1 > max(v2, v3)

action = 1

elseif v2 > max(v1, v3)

action = 2

else

action = 3

end

out[i, j] = action

else

out[i, j] = max(v1, v2, v3)

end

end

end

end

function update_bellman(cp, v; ret_policy = false)

out = similar(v)

update_bellman!(cp, v, out, ret_policy = ret_policy)

return out

end

function get_greedy!(cp, v, out)

update_bellman!(cp, v, out, ret_policy = true)

end

function get_greedy(cp, v)

update_bellman(cp, v, ret_policy = true)

end

get_greedy (generic function with 1 method)

The code defines

a named tuple

CareerWorkerProblemthatencapsulates all the details of a particular parameterization

implements the Bellman operator \(T\)

In this model, \(T\) is defined by \(Tv(\theta, \epsilon) = \max\{I, II, III\}\), where \(I\), \(II\) and \(III\) are as given in (33.2), replacing \(V\) with \(v\).

The default probability distributions in CareerWorkerProblem correspond to discrete uniform distributions (see the Beta-binomial figure).

In fact all our default settings correspond to the version studied in [LS18], section 6.5.

Hence we can reproduce figures 6.5.1 and 6.5.2 shown there, which exhibit the value function and optimal policy respectively.

Here’s the value function

wp = CareerWorkerProblem()

v_init = fill(100.0, wp.N, wp.N)

func(x) = update_bellman(wp, x)

sol = fixedpoint(func, v_init)

v = sol.zero

plot(linetype = :surface, wp.theta, wp.epsilon, transpose(v),

xlabel = L"\theta",

ylabel = L"\epsilon",

seriescolor = :plasma, gridalpha = 1)

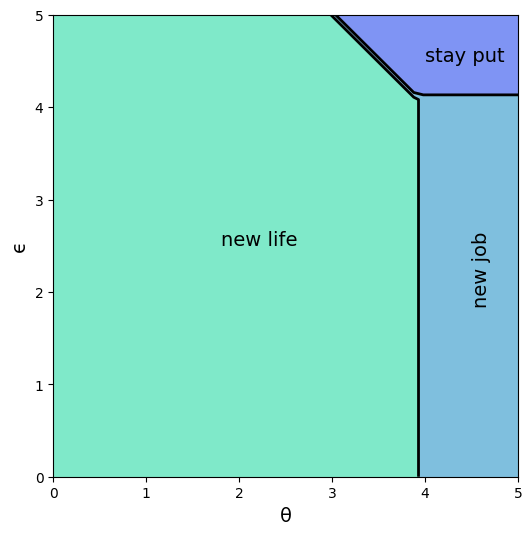

The optimal policy can be represented as follows (see Exercise 3 for code).

Interpretation:

If both job and career are poor or mediocre, the worker will experiment with new job and new career.

If career is sufficiently good, the worker will hold it and experiment with new jobs until a sufficiently good one is found.

If both job and career are good, the worker will stay put.

Notice that the worker will always hold on to a sufficiently good career, but not necessarily hold on to even the best paying job.

The reason is that high lifetime wages require both variables to be large, and the worker cannot change careers without changing jobs.

Sometimes a good job must be sacrificed in order to change to a better career.

33.3. Exercises#

33.3.1. Exercise 1#

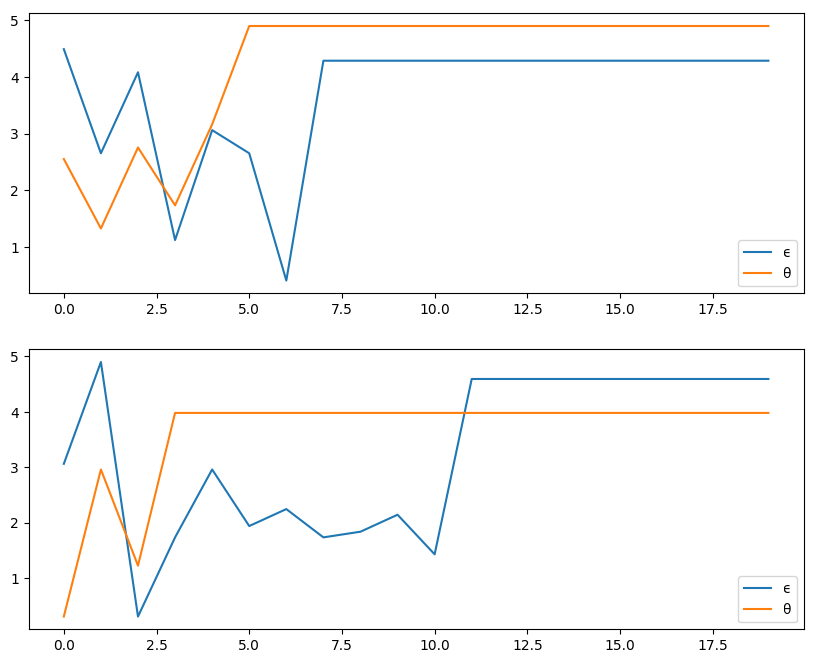

Using the default parameterization in the CareerWorkerProblem,

generate and plot typical sample paths for \(\theta\) and \(\epsilon\)

when the worker follows the optimal policy.

In particular, modulo randomness, reproduce the following figure (where the horizontal axis represents time)

Hint: To generate the draws from the distributions \(F\) and \(G\), you can use the Categorical distribution from the Distributions package.

33.3.2. Exercise 2#

Let’s now consider how long it takes for the worker to settle down to a permanent job, given a starting point of \((\theta, \epsilon) = (0, 0)\).

In other words, we want to study the distribution of the random variable

Evidently, the worker’s job becomes permanent if and only if \((\theta_t, \epsilon_t)\) enters the “stay put” region of \((\theta, \epsilon)\) space.

Letting \(S\) denote this region, \(T^*\) can be expressed as the first passage time to \(S\) under the optimal policy:

Collect 25,000 draws of this random variable and compute the median (which should be about 7).

Repeat the exercise with \(\beta=0.99\) and interpret the change.

33.3.3. Exercise 3#

As best you can, reproduce the figure showing the optimal policy.

Hint: The get_greedy() method returns a representation of the optimal

policy where values 1, 2 and 3 correspond to “stay put”, “new job” and “new life” respectively. Use this and the plots functions (e.g., contour, contour!) to produce the different shadings.

Now set G_a = G_b = 100 and generate a new figure with these parameters. Interpret.

33.4. Solutions#

33.4.1. Exercise 1#

wp = CareerWorkerProblem()

function solve_wp(wp)

v_init = fill(100.0, wp.N, wp.N)

func(x) = update_bellman(wp, x)

sol = fixedpoint(func, v_init)

v = sol.zero

optimal_policy = get_greedy(wp, v)

return v, optimal_policy

end

v, optimal_policy = solve_wp(wp)

F = Categorical(wp.F_probs)

G = Categorical(wp.G_probs)

function gen_path(T = 20)

i = j = 1

theta_ind = Int[]

epsilon_ind = Int[]

for t in 1:T

# do nothing if stay put

if optimal_policy[i, j] == 2 # new job

j = rand(G)

elseif optimal_policy[i, j] == 3 # new life

i, j = rand(F), rand(G)

end

push!(theta_ind, i)

push!(epsilon_ind, j)

end

return wp.theta[theta_ind], wp.epsilon[epsilon_ind]

end

Random.seed!(42)

plot_array = Any[]

for i in 1:2

theta_path, epsilon_path = gen_path()

plt = plot(epsilon_path, label = L"\epsilon")

plot!(plt, theta_path, label = L"\theta")

plot!(plt, legend = :bottomright)

push!(plot_array, plt)

end

plot(plot_array..., layout = (2, 1))

33.4.2. Exercise 2#

The median for the original parameterization can be computed as follows

function gen_first_passage_time(optimal_policy)

t = 0

i = j = 1

while true

if optimal_policy[i, j] == 1 # Stay put

return t

elseif optimal_policy[i, j] == 2 # New job

j = rand(G)[1]

else # New life

i, j = rand(F)[1], rand(G)[1]

end

t += 1

end

end

Random.seed!(42)

M = 25000

samples = zeros(M)

for i in 1:M

samples[i] = gen_first_passage_time(optimal_policy)

end

print(median(samples))

7.0

To compute the median with \(\beta=0.99\) instead of the default value \(\beta=0.95\), replace wp=CareerWorkerProblem() with wp=CareerWorkerProblem(beta=0.99).

The medians are subject to randomness, but should be about 7 and 14 respectively. Not surprisingly, more patient workers will wait longer to settle down to their final job.

wp2 = CareerWorkerProblem(beta = 0.99)

v2, optimal_policy2 = solve_wp(wp2)

Random.seed!(42)

samples2 = zeros(M)

for i in 1:M

samples2[i] = gen_first_passage_time(optimal_policy2)

end

print(median(samples2))

14.0

33.4.3. Exercise 3#

Here’s the code to reproduce the original figure

wp = CareerWorkerProblem();

v, optimal_policy = solve_wp(wp)

lvls = [0.5, 1.5, 2.5, 3.5]

x_grid = range(0, 5, length = 50)

y_grid = range(0, 5, length = 50)

contour(x_grid, y_grid, optimal_policy', fill = true, levels = lvls,

color = :Blues,

fillalpha = 1, cbar = false)

contour!(xlabel = L"\theta", ylabel = L"\epsilon")

annotate!([(1.8, 2.5, text("new life", 14, :white, :center))])

annotate!([(4.5, 2.5, text("new job", 14, :center))])

annotate!([(4.0, 4.5, text("stay put", 14, :center))])

Now, we need only swap out for the new parameters

wp = CareerWorkerProblem(G_a = 100.0, G_b = 100.0); # use new params

v, optimal_policy = solve_wp(wp)

lvls = [0.5, 1.5, 2.5, 3.5]

x_grid = range(0, 5, length = 50)

y_grid = range(0, 5, length = 50)

contour(x_grid, y_grid, optimal_policy', fill = true, levels = lvls,

color = :Blues,

fillalpha = 1, cbar = false)

contour!(xlabel = L"\theta", ylabel = L"\epsilon")

annotate!([(1.8, 2.5, text("new life", 14, :white, :center))])

annotate!([(4.5, 2.5, text("new job", 14, :center))])

annotate!([(4.0, 4.5, text("stay put", 14, :center))])

You will see that the region for which the worker will stay put has grown because the distribution for \(\epsilon\) has become more concentrated around the mean, making high-paying jobs less realistic.